What Happens During Reverse Mortgage Counseling?

If you are considering a home equity conversion mortgage (HECM), you’ll need counseling before applying for the loan. Even if you have researched all of the requirements for this loan, counseling is mandatory to help you understand the implications of this mortgage and how they affect your financial situation. In this article, we’ll look at how to find reverse mortgage counseling and what you can expect in the process.

What Is Reverse Mortgage Counseling?

Reverse mortgage counseling is required for homeowners considering a HECM — a reverse mortgage backed by the federal government. This mortgage is a complex financial product, so homeowners must complete counseling with an approved counselor.

By having a counseling session, homeowners can understand how the product works and assess whether it is the best solution for their financial situation. This is also known as FHA reverse mortgage counseling, as the Federal Housing Administration (FHA) insures HECMs.

Counselors must cover specific topics during the session, including reverse mortgage features and costs, tax and financial implications, and reverse mortgage scam education.

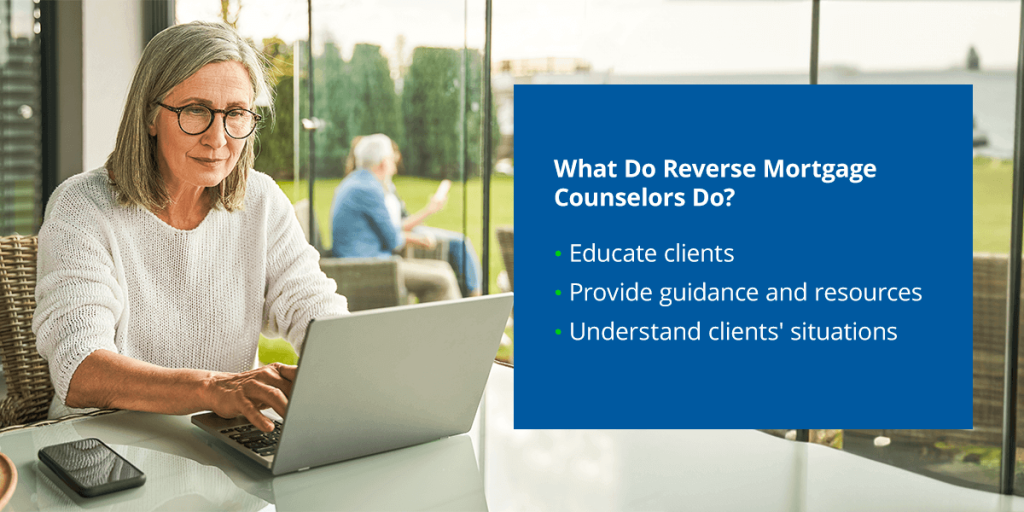

What Do Reverse Mortgage Counselors Do?

Reverse mortgage counselors have numerous responsibilities toward their clients.

- Educate clients: The counselor must educate homeowners on the reverse mortgage features, whether it is appropriate for them and what other financial options may meet their needs.

- Provide guidance and resources: Homeowners need guidance from counselors to make an informed decision. Before your counseling session, the counselor should provide you with a pre-counseling informational packet containing a copy of “Preparing for Your Counseling Session,” a list of loan comparisons, a copy of the total annual loan cost, a loan amortization schedule showing the costs over the loan’s lifetime, and a copy of “Use Your Home to Stay at Home” from the National Council on Aging.

- Understand clients’ situations: A reverse mortgage counselor must familiarize themselves with your financial situation and unique needs and discuss reverse mortgage products and other financial and social service housing options within the context of your situation. While the counselor can advise you, they cannot tell you whether or not to process the loan or tell you which product to use.

How Much Does Counseling Cost?

Reverse mortgage counselors can charge a fee that is both reasonable and customary. This fee is usually $125-$150. Lenders cannot pay this fee for clients to ensure they remain impartial. If the cost is unaffordable, you can contact the counseling agency to request hardship approval, allowing you to pay a reduced rate.

The Department of Housing and Urban Development (HUD) authorizes counselors to waive the fee for homeowners who meet the following criteria:

- Fall below 200% of the federal poverty level

- Are delinquent on their mortgage

- Have defaulted on their debt

- Are experiencing homelessness

Reverse Mortgage Steps

Once you decide to go ahead with a reverse mortgage, you’ll need to follow a five-step process. Homeowners do not need to meet credit score criteria for the mortgage, but the lender will evaluate your financial standing to ensure you are not delinquent on federal debt.

- Initial application: You will complete an initial application with a lender. The application will detail necessary information such as the fees, interest rates and loan proceeds. You can still cancel the application at any point in the process without penalty.

- Reverse mortgage counseling: You will then have a counseling session with a federally insured counseling agency to decide if it is the right option.

- Counseling certification: After counseling, you will meet with a notary to sign a certificate stating you completed reverse mortgage counseling. Then, you will complete other paperwork, such as documentation of income, assets, credit history and additional liens.

- Appraisal: You need a home appraisal when you submit your documentation, counseling certificate and signed application. An appraiser may also take pictures of your home, measure the square footage and examine recent renovations and maintenance.

- Underwriting: The appraiser will then hand the report to the underwriter, who will analyze your credit risk. If there are any issues, the underwriter will work with you to help you correct them.

- Closing: Once you have loan approval, you will have a date scheduled to close the loan with an attorney or title agent. At this stage, you sign the final documents for the reverse mortgage loan.

- Funding: In the final step of the process, you will authorize the loan application. You can receive the funds as a lump sum, monthly payments or credit.

During the Reverse Mortgage Counseling Session

A reverse mortgage counseling session typically takes one hour. Even after your session, your counselor will continue to support you. During the session, you can expect to discuss the following:

- Your financial needs and situation

- Features of a reverse mortgage

- Your responsibilities when you have a reverse mortgage

- Costs of a reverse mortgage

- Reverse mortgage financial and tax implications

- Alternatives to a reverse mortgage loan

- Reverse mortgage scams and financial elder abuse

What Is the Difference Between a Reverse Mortgage and a Home Equity Loan?

As a homeowner who’s 62 or older, you have other alternatives to a reverse mortgage, including home equity loans and home equity lines of credit (HELOCs). While all three options allow you to convert your home equity to cash, key differences exist.

The disbursement of each loan differs in the following ways:

- Reverse mortgages, you receive either monthly payments, lump-sum payments or a line of credit. You can also choose a combination of these.

- A home equity loan is disbursed as a lump sum payment.

- A HELOC is disbursed to clients as they need the funds up to a pre-approved credit limit.

Each loan comes with different repayment terms:

- Reverse mortgage loan repayment is due once a homeowner becomes delinquent on taxes or home insurance, decides to sell their house or fails to upkeep the home.

- A home equity loan involves monthly repayment over a specific period with a fixed interest rate.

- A HELOC requires payments to cover the interest during the draw period, and the payments increase during the repayment period based on the balance and variable interest rate.

The following age and equity requirements apply:

- Reverse mortgage applicants must be at least 62 years old and have sufficient equity in their home.

- Home equity loan has no age requirements, but you must have a minimum of 20% equity on your home.

- HELOCs have no minimum age requirement, and you must have a minimum home equity of 20%.

Your credit and income status will affect your application in the following ways:

- A reverse mortgage loan has no credit score requirements, but some lenders will check that you pay your property taxes and insurance.

- Home equity loans require a good credit score and proof of a steady income.

- HELOCs require good credit and sufficient, steady income to cover financial obligations.

Speak to Florida Reverse Mortgage Consultants at Senior Lending Corporation

A reverse mortgage loan can give you the funds to improve your retirement. A reverse mortgage loan is a fairly complex financial product, which is why counseling is essential to help you make an informed decision.

Have questions about reverse mortgage counseling requirements or other parts of this process? At Senior Lending Corporation, our expert team is here to help you every step of the way. Contact us today for reverse mortgage counseling in Florida.